- Bianco’s analysis unveils soaring flows into Bitcoin ETFs despite Grayscale’s consistent outflows due to fee discrepancies.

- The demographic breakdown reveals a stark contrast between short-term traders and long-term allocators in the Bitcoin ETF market.

- The analyst warns of potential market risks, citing regulatory restrictions and historical parallels, signaling caution in the current ETF landscape.

In a pivotal move, renowned crypto analyst Jim Bianco delved into the dynamics of spot Bitcoin ETFs, shedding light on their intricate workings. In a recent X post, the provided insights encapsulated within five illustrative charts, offering a comprehensive analysis of the market trends and the potential impact of spot Bitcoin ETFs on the crypto landscape.

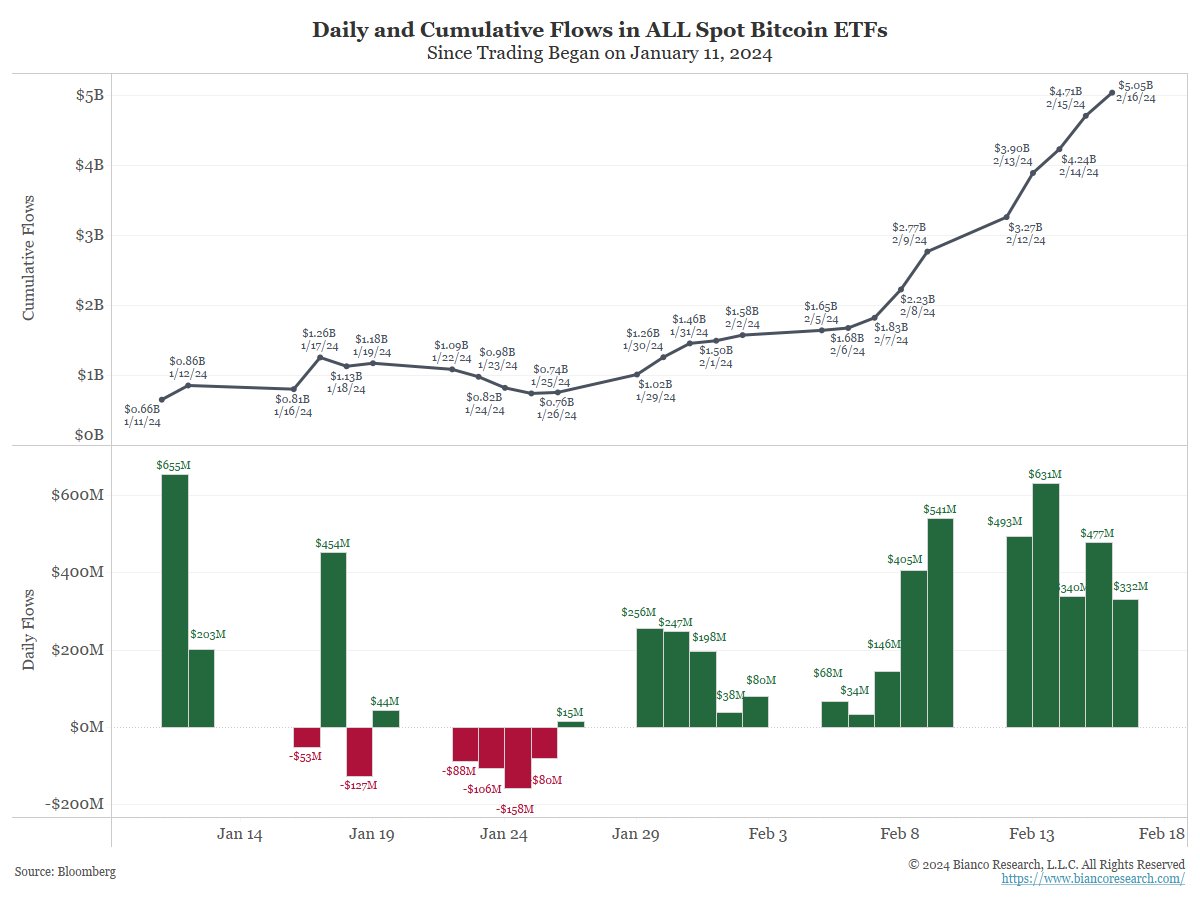

Eleven spot Bitcoin ETFs commenced trading on January 11, a significant event marking the entry of Bitcoin into the ETF realm. Notably, ten of these ETFs began with minimal assets, while Grayscale, having converted from a closed-end fund, initiated with nearly $29 billion in assets.

The influx of capital into spot Bitcoin ETFs has been staggering, surpassing records for the ETF industry within the initial weeks. Flows, excluding Grayscale, have averaged over $500 million daily over recent trading sessions, dwarfing prior industry estimates.

However, Grayscale’s singular position has faced challenges, experiencing daily outflows attributed to two primary factors. Firstly, competing funds slashing fees to negligible levels (0 to 12 bps) have undermined Grayscale’s comparatively high 150 bps fee structure. Additionally, the conversion of Grayscale from a closed-end fund to an ETF on January 11 marked a strategic shift for investors, leading to the closure of arbitrage trades initiated during its discount phase.

Bianco also delved into the demographics of spot Bitcoin ETF investors, distinguishing between “trader ETFs” and “allocator ETFs.” Trader ETFs, characterized by frequent trading activity, primarily attract speculative investors, whereas allocator ETFs, dominated by long-term holders, prioritize asset accumulation irrespective of market fluctuations.

In another post, Bianco revealed that the cumulative flows in these categories, as depicted in the data, unveil a striking disparity in investment patterns. Trader ETFs have garnered $68 billion in total flows over six years, while allocator ETFs have seen a substantial $750 billion inflow during the same period, indicating a preference for long-term investment strategies.

Vanguard’s absence from the spot Bitcoin ETF market is notable, suggesting that major allocator entities refrain from endorsing these products. This underscores the likelihood that short-term traders predominantly drive spot Bitcoin ETF investments.

Bianco parallels historical market events and highlights potential risks associated with the current ETF landscape. He warns of the consequences of mass sell-offs in spot Bitcoin ETFs, exacerbated by regulatory restrictions on in-kind redemptions, which could trigger rapid market downturns akin to past volatility episodes.

The focus on short-term gains within the crypto space, coupled with the integration of traditional finance, raises concerns about potential regulatory interventions in the future. Bianco’s analysis serves as a sobering reminder of the fragility inherent in the current market dynamics and the implications for traditional finance and the broader cryptocurrency ecosystem.