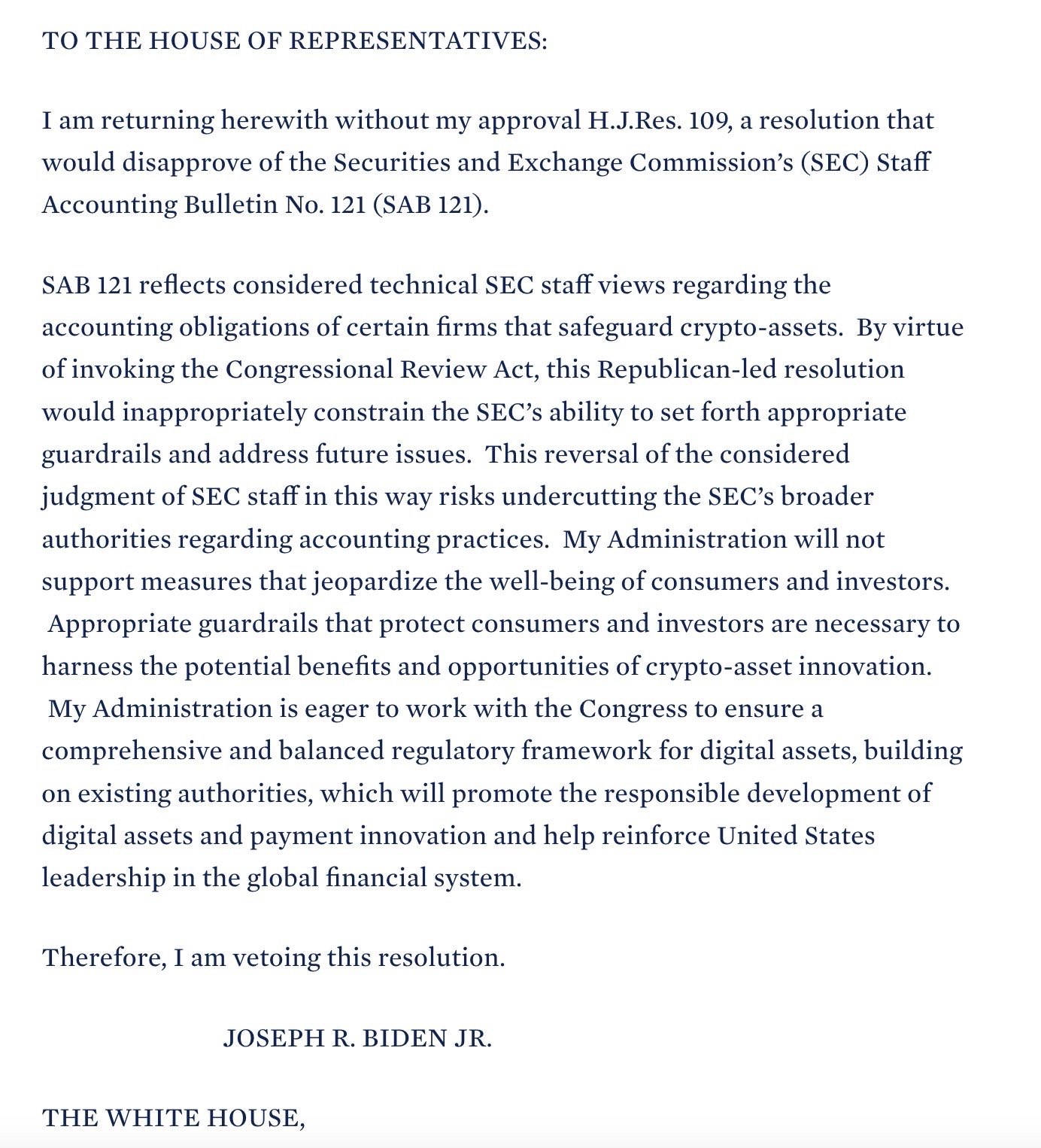

- Biden rejects House resolution to overturn SEC’s SAB 121, citing consumer and investor protection.

- Critics argue that SAB 121 complicates financial institutions’ crypto dealings, and Biden supports the SEC’s authority.

- Banking groups and Congress urged him to sign the resolution overturning SEC’s SAB 121.

President Joe Biden stated that he had signed a joint resolution of the House and Representatives, vetoing a resolution that would have revoked the SEC’s Staff Accounting Bulletin 121 (SAB 121).

SAB 121 is a contentious SEC accounting rule that compels financial firms holding customer cryptocurrencies to record the assets on their balance sheets. Critics claim that the advice makes engaging with Bitcoin startups extremely difficult for financial institutions.

Biden highlighted the rule’s significance in safeguarding the public, stating, “My Administration will not support measures that jeopardize the well-being of consumers and investors.”

Notice Regarding Biden’s Veto

On May 8, the Biden administration sent a notification suggesting that President Joe Biden would veto the resolution if the Senate approved it. The administration has warned against eliminating SAB 121, which would jeopardize the SEC’s efforts to protect investors and the financial system.

Congressman Urges Quick Senate Action on FIT21 Before ElectionsThe House of Representatives passed the resolution, with a majority of legislators voting in favor. However, a Senate vote is insufficient to overturn a presidential veto, which requires a two-thirds majority vote in both chambers.

SAB Disputes

SAB 121 requires financial institutions and businesses to maintain balance sheets for customer assets. The American Bankers Association (ABA) opposes this, claiming that it makes it expensive for banks to serve as spot Bitcoin ETF custodians and fails to distinguish between crypto and traditional assets on public ledgers. The ABA seeks changes rather than a total revocation.

Lawmakers Urge to Biden’s Administration for Repeal

The American Bankers Association and three other organizations urged President Biden to sign a joint resolution overturning a Securities and Exchange Commission staff accounting bulletin that alters how banks and other publicly traded entities are expected to account for digital assets held in custody.

In a joint letter, the groups stated that the SEC approved the bulletin without consulting prudential authorities or inviting public opinion. It differs from the standard accounting view of custodial assets as off-balance-sheet assets.