Are Stablecoins Reshaping Global Monetary Policy?

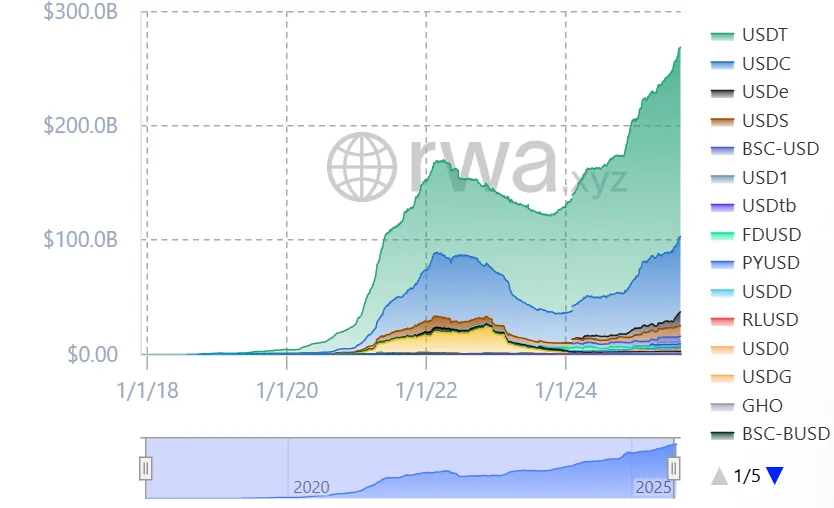

Stablecoins have steadily gained momentum in the cryptocurrency ecosystem. These digital assets, pegged to the U.S. dollar, offer stability, thus driving mass adoption. By mid-2025, the global stablecoins market had surpassed $270 billion and will potentially cross $2 trillion by 2028.

According to market observers, Morgan Stanley predicted that stablecoins could reach $1.2 trillion by 2028, while Standard Chartered expects $2 trillion, and brokerage Bernstein envisions as much as $4 trillion by 2035. If these estimates materialise, the sector’s demand for short‑term government debt could expand dramatically.

Growing demand for digital tokens

Apart from Morgan Stanley, other banks like Bank of America and Citigroup have indicated that they may issue their own tokens once legal details are finalised. Bank of America CEO Brian Moynihan asserted that the bank will respond to client demand, and talks for a possible stablecoin are underway. Meanwhile, Citigroup CEO Jane Fraser called a Citi stablecoin “a good opportunity”.

On the other hand, banks caution that holding stablecoins could require extra capital and regulatory guidance. Central banks are concerned about the monetary effects. Kansas City Fed economists caution that bank deposits could decline if consumers shift money to stablecoins.

They estimate that lending could decrease by 50 cents and Treasury holdings could increase by 30 cents for every dollar shifted into stablecoins, thus supporting government borrowing but constraining household and business lending.

Cross-border capital analysts note that stablecoins transform medium‑term Treasury bills into instantly spendable assets. While that may boost liquidity in financial markets, it does not create new credit. Thus, the overall impact on the money supply could be muted, but the shift could complicate the Federal Reserve’s management of short‑term interest rates and transmission of monetary policy.

European asset managers worry that U.S. stablecoin policy might have global repercussions. Vincent Mortier of Amundi warned that a surge in dollar‑pegged stablecoins could destabilise international payments and undermine other currencies.

Italy’s finance minister, Giancarlo Giorgetti, said digital dollars could erode European monetary sovereignty. The Bank for International Settlements has also cautioned that stablecoins could encourage capital flight from emerging markets. Such concerns could prompt other nations to develop their own digital tokens or impose restrictions on foreign‑issued stablecoins.

Related: Stablecoins Don’t Boost Treasury Demand, Peter Schiff Warns

Global Outlook on Monetary Policy

Stablecoins were initially developed to allow cryptocurrency traders to have a medium of exchange pegged to currencies. Most stablecoin issuers currently hold large amounts of U.S. Treasury bills since regulations only allow a limited range of collateral assets.

Economists at the Federal Reserve Bank of Kansas City estimate that stablecoin issuers hold about $125 billion in Treasury bills that account for less than 2% of the $6 trillion U.S. bill market. Still, it exceeds the holdings of many hedge funds and even some foreign governments.

This demand is growing while traditional foreign buyers are reducing their positions. Over the past decade, their share of U.S. Treasuries has fallen from roughly 25% to around 6%.

This surge has led governments and financial authorities worldwide to develop regulatory frameworks to promote stability, security, and integration into the existing monetary systems.

United States: The GENIUS Act and Its Implications

Yie‑Hsin Hung of State Street Global Advisors said around 80% of stablecoin reserves are invested in U.S. Treasuries or repurchase agreements, while Mark Cabana of Bank of America predicted that the Treasury may need to adjust its issuance strategy to accommodate that demand.

With U.S. government debt topping $37 trillion, Washington is issuing more short‑term Treasury bills to finance the deficit along with stablecoin issuers, who have emerged to be potential buyers. Further, the GENIUS Act mandates that stablecoin issuers maintain full backing with high-quality liquid assets, such as U.S. Treasury bills, and undergo regular audits. It also prohibits issuers from paying interest directly to customers, aiming to prevent potential disruptions in the banking sector.

Globally, most stablecoins are linked to the U.S. dollar, reflecting its dominance in trade. The major dominator, Tether’s USDT token, accounts for roughly 68% of the market, while Circle’s USDC accounts for about 24%, giving the pair a combined market share above 90%.

In addition, CoinShares found that almost half of users in emerging markets save in digital dollars, and more than 80% of all stablecoin transactions occur overseas. Moreover, stablecoins are already widely used outside the United States.

European Union: MiCA Regulation and Its Reach

The Markets in Crypto-assets (MiCA) regulation of the European Union, effective as of January 2025, offers a comprehensive legal framework covering cryptocurrencies in the EU. MiCA classifies stablecoins as e-money tokens and subjects them to stricter requirements, full reserve backing, licensing, and regular disclosures.

Despite a practical regulatory framework, the European Central Bank has stated that privately issued stablecoins are risky as they interfere with monetary policies and financial stability. This has raised the debate regarding the creation of a digital euro to supplement the measures implemented.

Hong Kong: A Progressive Approach to Stablecoin Regulation

In Hong Kong, authorities enacted the Stablecoins Ordinance on August 1, 2025, which introduced a licensing framework for fiat-referenced stablecoin issuers. Implemented by the Hong Kong Monetary Authority (HKMA), issuers are supposed to follow strict guidelines regarding maintaining reserves, transparency, and protecting the consumer.

It is an effective way of being proactive in ensuring that Hong Kong becomes a center of digital asset innovation in the Asian Region, and local and international players in the stablecoin market will be attracted.

Japan: Embracing Stablecoins with Caution

Japan has made considerable moves towards introducing stablecoins into its payments and financial system. Japan’s amended Payment Services Act introduces “e‑money stablecoins”, issued by domestic banks or trust banks and backed one‑to‑one with reserves and foreign issuers must hold equivalent reserves within Japan.

In August 2025, JPYC Inc. was issued a funds transfer service provider license and became authorized to issue the first yen-pegged stablecoin, backed by bank deposits and government bonds. Furthermore, the Financial Services Agency (FSA) has revised the Payment Services Act to support the stablecoin issuers and regulate their activity in an open and safe environment.

China: Shifting Policies Towards Digital Currency Integration

China, which had an iron hand against cryptocurrency, has slightly loosened its hold on the digital asset ecosystem and is reportedly considering adopting yuan-backed stablecoins to encourage the expansion of the Chinese currency. Such action would overturn earlier strict policies on digital assets, indicating the interest of locals in the use of digital currencies.

The People’s Bank of China has promoted the idea of the digital yuan (e-CNY), which can be implemented for better access, thus limiting the use of standard financial systems. Chinese authorities see domestic tokens as a means of promoting their currency to the world, as more than 99% of existing stablecoins are pegged to the U.S dollar.

Related: China’s Stablecoin Push Challenges U.S. Dollar Dominance

United Kingdom: Draft Legislation and Regulatory Developments

In the UK, the government has issued draft legislation under the Financial Services and Markets Act 2000, which proposes to regulate fiat-referenced stablecoins as a new regulated activity. The Financial Conduct Authority (FCA) has said that it will treat qualifying stablecoins as money-like products rather than investment products, providing consumer protection and financial stability. These trends indicate the UK’s willingness to promote innovation in the digital assets sector while preserving a safe and regulated market.

Brazil: Adapting to the Rise of Stablecoins

The Brazilian central bank is enforcing a Virtual Assets Act, which includes regulating stablecoins. Stablecoin usage in the country has grown considerably, with transactions involving cross-border payments and remittances. Brazil is weighing whether to loosen some restrictions on self-hosted wallets and cross-border transfers that have been proposed so far. This would foster innovation while balancing it with regulations.

United Arab Emirates: Central Bank’s Stablecoin Regulations

Beginning in August 2025, the UAE Central Bank implemented rules that allowed merchants to accept only licensed Dirham Payment Tokens (DPTs) in the country. This step guarantees that the stablecoins that work in the UAE are undergoing centralized regulation, assuring financial stability and consumer protection. Furthermore, the Abu Dhabi Global Market (ADGM) has established a governing structure regarding the release of tokenised fiat currency, further enhancing the UAE as one of the most successful fintech hubs in the Middle East.

Singapore: Regulating Stablecoin Issuance

Singapore’s Monetary Authority (MAS) introduced a stablecoin framework to ensure single-currency stablecoins pegged to the Singapore dollar or other major currencies to maintain value stability.

Issuers must possess sufficient reserve assets, be redeemable in time, possess adequate capital, and make transparent disclosures. Non-bank issuers with more than $5 million in circulation require a license. This method is in line with an international trend of more restrictive oversight and licensing of stablecoins.

Switzerland: FINMA’s Stablecoin Guidance

Switzerland has not yet issued a particular stablecoin law. Instead, it relies on current financial regulations and regulatory advice by its financial regulator, FINMA. In July 2024, FINMA suggested two critical rules: Any bank guarantee of a stablecoin needs to meet strict conditions (it is possible to be an issuer without a banking license), and issuers should check the identity of all holders of a stablecoin to prevent its anonymous use. This position reflects the global attempts to tighten the regulation of stablecoins.