Blockchain data intelligence firm Glassnode has stated that liquidity in the digital asset market “continues to dry up”. Liquidity, volatility, and volume continue to fall across the digital asset market, with many metrics returning to pre-bull levels in 2020.

In a recent tweet, Glassnode highlighted the current condition of the market:

Liquidity is a key indicator of how well financial markets are functioning. It refers to how easily assets could be bought or sold—and when it dries up, it could be disruptive. On-chain and off-chain volumes have reached historical lows, indicating less activity and trading than in the past.

In spite of the decrease in liquidity, the market appears to prefer “HODLing”. This means many investors prefer holding on to their digital assets rather than actively trading them.

Further the report stated, “whilst HODLing remains the market preference, a significant proportion of the supply is teetering on the edge of falling into a significant unrealized loss”. This means that the value of their holdings may have fallen below what they paid for them, but they haven’t sold them yet, causing uncertainty and pressure on holders to decide whether to sell or hold.

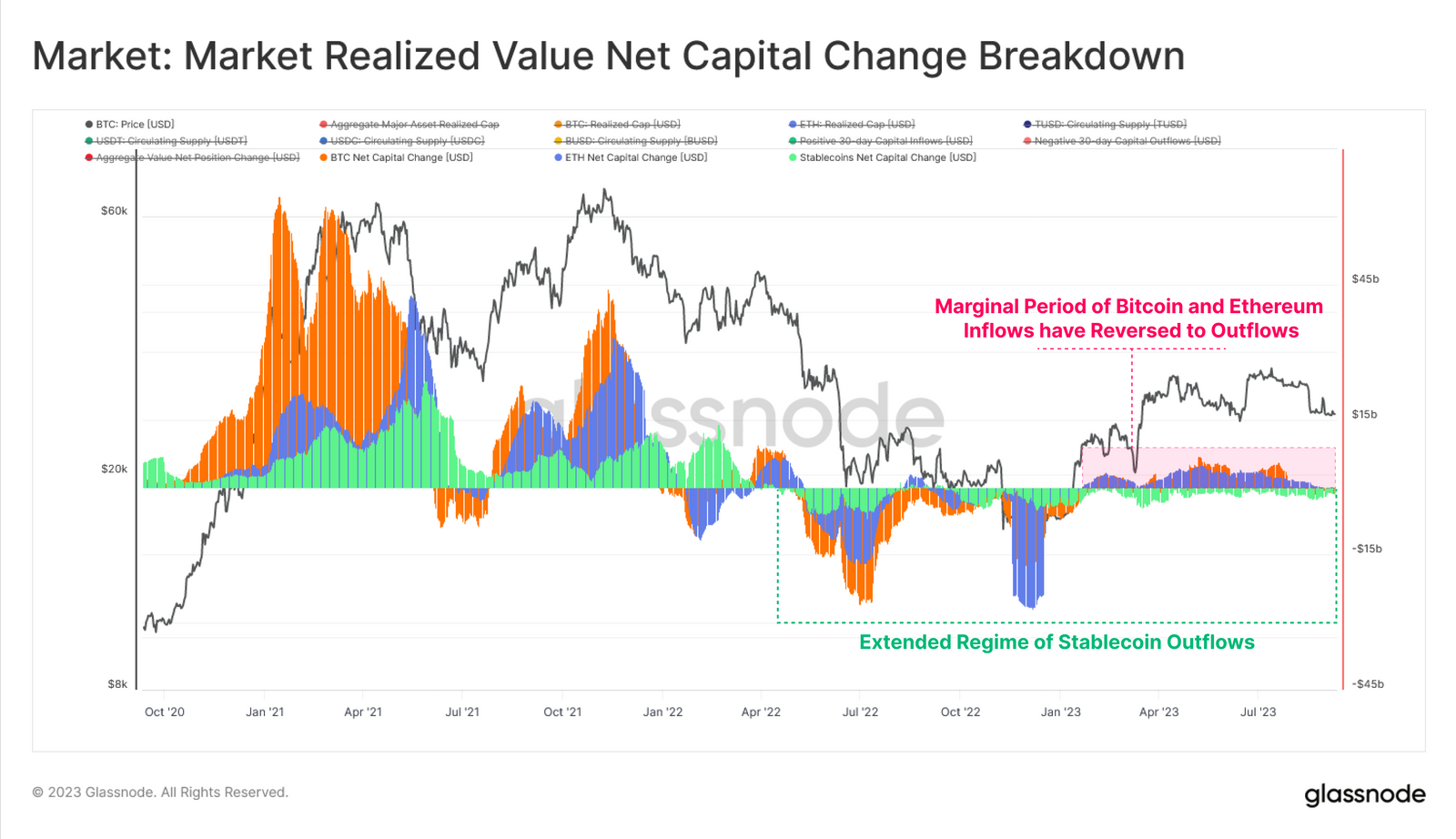

Glassnode reported that except for Tether (USDT), there has been a sharp decline in the supply of stablecoins since April 2022. It is reportedly due to the redemption that began following the collapse of LUNA-UST. Furthermore, both Bitcoin and Ethereum have seen a net inflow of capital since the beginning of the year, with their Realised Caps increasing by up to $6.8B/mth (BTC) and $4.8B/mth, respectively, as shown in the image.

Stablecoin supply has been steadily decreasing, totaling $43 billion, a 26% decrease from the peak in March 2022. It could be due to two major factors: the bear market’s adverse conditions, which are causing capital to exit, and the growing opportunity cost associated with non-yielding stablecoins, especially in light of higher interest rates elsewhere.

Since reaching cycle lows in November 2022, the supply of USDT (Tether) has actually increased by $13.3 billion. Additionally, the USDC has experienced a nearly equivalent and opposing decline of -$16.7 billion as a result of US-based institutions reallocating capital to higher-interest-rate markets. And, BUSD (Binance USD) has dropped by $20.4 billion, or 89%, as a result of the issuer, Paxos, switching to a redemption-only mode in response to Securities and Exchange Commission (SEC) enforcement actions.

The report also emphasised that the proportion of wealth held in the most active and liquid segment of the market, the ‘Hot Supply’ cohort (coins moved within the last week), is at an all-time low. This implies that very few coins older than one week are currently transacting.

Furthermore, futures trading volumes have reached historic lows in 2023, while options markets have seen increased volumes. This could be due to the market preferring to express itself through the leverage and capital efficiency of options during a period of tighter overall liquidity conditions.