Strategy’s Bitcoin Premium Vanishes as mNAV Falls Below 1

- Strategy’s mNAV below 1 makes new equity issuance potentially dilutive for holders.

- STRC trades far below par as annual dividend obligations tighten Strategy’s cash buffer.

- Metaplanet and Nakamoto trade below parity as Bitcoin treasury valuations weaken.

Strategy’s long-standing premium over its Bitcoin holdings has now disappeared, signaling a clear shift in how investors view the company’s bold crypto-focused approach. On Friday, its enterprise mNAV slipped below 1, meaning the company’s overall market value dropped beneath the value of the Bitcoin it holds. MSTR shares fell to $82.16 during the day and edged down further to around $81.80 after hours. At the same time, Bitcoin hovered near $59,560 after briefly dipping to $58,000 the day before.

This change effectively wipes out the extra value investors once placed on Strategy’s Bitcoin-heavy strategy. It also puts the company below a key level that management has relied on when issuing new shares to fund more Bitcoin purchases. With that option now less attractive, attention is turning to how Strategy might adjust if the discount continues.

MSTR Drops Below Management’s Accretive Threshold

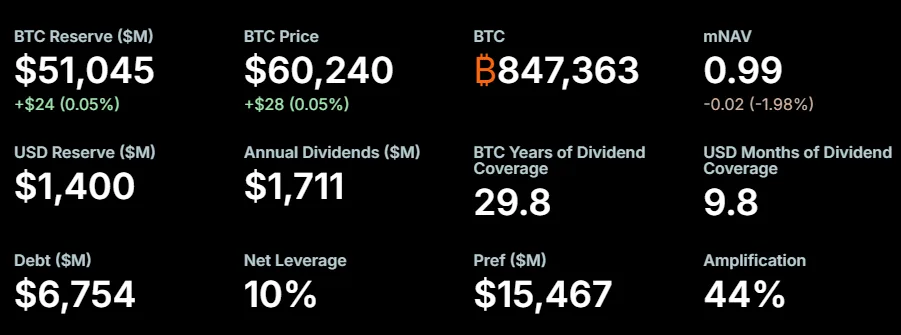

Enterprise mNAV compares Strategy’s total market value to its Bitcoin holdings after factoring in debt, cash, and preferred shares. When the ratio falls below 1, it shows the company is trading at less than the value of its Bitcoin reserves.

According to Wu Blockchain, Strategy’s mNAV is now “well below the roughly 1.22x threshold” that management previously considered necessary for issuing new shares without diluting value. That level was seen as the point where raising capital through equity would still benefit shareholders by increasing Bitcoin exposure per share.

Dropping below that mark makes things more complicated. Issuing new shares at this level could actually reduce value for existing investors instead of adding to it. Because of this, the company may need to rethink how it manages its capital and maintains investor confidence.

Possible moves include building up cash reserves, selling some of its Bitcoin, or buying back shares to support the stock price. Each of these options could offer more immediate benefits than issuing discounted shares to buy more Bitcoin.

Strategy’s own guidelines also limit Bitcoin purchases funded by equity when mNAV falls below 1. In this situation, the company may focus more on using cash for share buybacks and reviewing its dividend commitments tied to preferred shares.

Related: Strategy Buys 22,337 BTC in $1.57B Treasury Expansion Plan

Preferred Share Costs Increase Financial Pressure

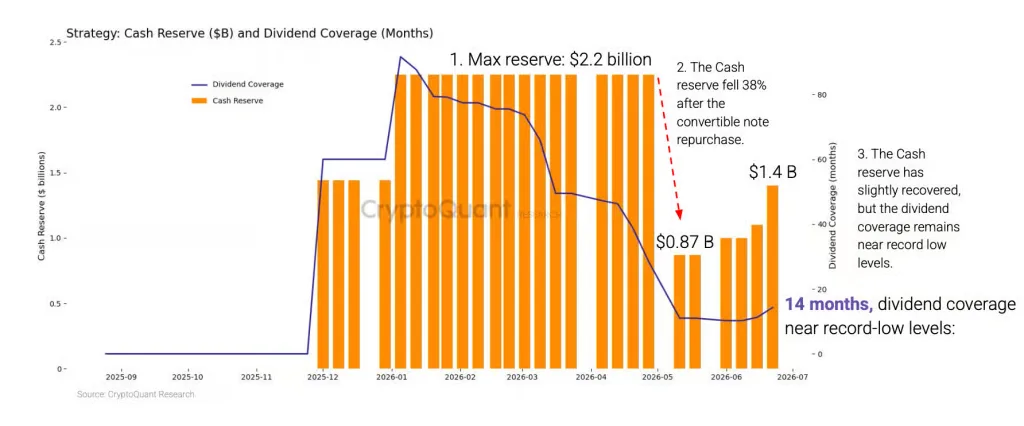

Strategy has leaned heavily on perpetual preferred shares, including STRC, to fund its Bitcoin buying plans through 2026. However, these come with a hefty price tag—about $1.2 billion in annual dividend payments.

Data from CryptoQuant shows the company holds roughly $1.4 billion in cash. That leaves only a narrow cushion above one year’s worth of dividend obligations, which could become a concern if market conditions worsen.

STRC shares have also taken a hit. They dropped to around $71.40 on Friday before closing at $74.72, nearly 26% below their intended $100 value. This decline reflects growing unease among investors about how sustainable the company’s funding approach really is.

Strategy isn’t alone in facing these challenges. Other firms with Bitcoin-heavy treasury strategies are seeing similar pressure. BitcoinTreasuries’ data shows Japan’s Metaplanet trading at an enterprise mNAV of about 0.90, while Nakamoto, backed by David Bailey, sits near 0.92.

On the other hand, Strive is still trading above parity, with an enterprise mNAV around 1.24. It uses SATA perpetual preferred shares to support its Bitcoin strategy, suggesting that investor confidence can vary widely even among companies using similar models.

For Strategy shareholders, a share buyback program could help narrow the gap between the company’s market value and its Bitcoin holdings. However, relying less on issuing new shares would also limit its main way of funding additional Bitcoin purchases.